Financial Inclusion in South Africa

Key Takeaways:

-

Access isn't enough: While 98% of South Africans have access to banking services, many still use their accounts primarily for basic transactions, not for long-term saving or investing. This indicates a gap between access to financial services and true financial inclusion.

-

Credit used for survival, not wealth creation: Many South Africans rely on credit to meet immediate needs, such as buying food, rather than using it as a tool for wealth-building. This short-term approach to credit limits their ability to save or invest for future stability.

-

Struggles with saving: A significant number of South Africans experience negative savings rates, which contributes to growing financial instability. Without savings, households become increasingly reliant on debt, which undermines their wealth-building potential.

-

Lack of financial protection through insurance: Most South Africans only have access to funeral cover, with few able to afford more comprehensive insurance products. This limited coverage leaves many exposed to financial shocks and further complicates efforts to build long-term wealth.

Financial Inclusion is critical for combating inequality and poverty.

There is significant economic inequality in South Africa, and access to financial services is essential for promoting economic growth and reducing poverty. Over the past two decades, the country has made considerable progress in increasing financial inclusion, with 98% of the population now formally served by financial services in 2023, according to Finmark Trust.

However, despite the high availability of banking services, the costs associated with credit, savings, and insurance products often prevent South Africans from fully participating in the financial system, limiting their ability to build wealth and protect themselves from financial shocks.

In this post, I explore the state of financial inclusion in South Africa, examining its impact on economic growth, the challenges posed by affordability, and the barriers to credit, savings, and insurance access.

Most South Africans have a bank account - but this is not enough

Over the past two decades, access to financial services in South Africa has improved significantly. In 2023, 98% of the population was formally served; a substantial increase from 68% in 2011. Being "formally served" means having access to financial services provided by regulated and recognized institutions, such as banks.

However, being formally served does not equate to full financial inclusion. Many South Africans use their bank accounts as little more than mailboxes to receive and withdraw their income. This reliance on cash remains prevalent, with Finmark Trust finding that 37% of people withdrawing their entire income from their bank accounts each month, and another 27% sometimes doing so. This highlights the gap between access to financial services and meaningful financial inclusion, which requires saving, investing, and leveraging financial tools for long-term stability and growth. Financial inclusion goes beyond having a bank account.

Having access to financial products such as credit, insurance, and savings can help individuals build wealth, smooth consumption, and weather unforeseen circumstances. Yet, many South Africans struggle to have savings or afford insurance. While the majority of adults have access to credit facilities they are often unable to use this as a tool to generate wealth, instead relying on credit to meet short-term needs.

South Africans use credit as a tool for survival, not wealth creation

Access to credit is important because it enables individuals to manage cash flows, access necessary goods and services, and navigate financial challenges. For people and businesses with fluctuating income, credit provides a cushion to cover expenses and manage cash flow more effectively.

Using credit responsibly contributes to building a good credit score, which can make it easier to qualify for better loan terms in the future, saving money and opening up new financial opportunities. Credit can also support wealth-building by enabling investments in assets such as homes or education, which can enhance earning potential and financial security. Additionally, credit acts as an emergency buffer, helping people manage unexpected expenses like medical bills or home repairs without needing immediate cash.

60% of South Africa’s adults have access to credit. However, the type of credit available differs significantly for people in different income brackets. The NCR’s Consumer Credit Report for the second quarter of 2024 shows that credit facilities, such as credit cards and store cards, are the most accessible options for South Africans earning less than R10,000 per month.

Although credit has the potential to be a wealth-building tool, access to asset-building credit—such as mortgages or developmental loans—is heavily skewed toward higher-income earners. For example, in June 2024, 99% of approved mortgages were given to South Africans earning more than R15,000 per month, while only 22% of developmental loans were granted to those earning less than R10,000 per month.

This disparity highlights the unequal access to wealth-building opportunities. Many South Africans rely on credit facilities for short-term needs rather than for long-term investments. In 2023, Finmark Trust found that most common reason for borrowing money in South Africa was to buy food, underscoring how credit is used primarily as a tool for survival rather than as a means to build wealth.

Most South Africans struggle to save, or to afford insurance

Despite the high level of access to banking services, savings remains a challenge for many South Africans. In 2023, South Africa’s household saving rate was negative, meaning households, on average, spent more than they earned. Instead of saving a portion of their disposable income, households drew down existing savings, sold assets, or took on debt to finance their consumption and living expenses.

This financial strain is evident in how savings are used: according to FinMark Trust, 27% of South Africans who saved in 2023 did so to buy food. This reliance on short-term savings for essential daily expenses rather than wealth-building or emergency funds underscores the precarious financial situation of many South African households.

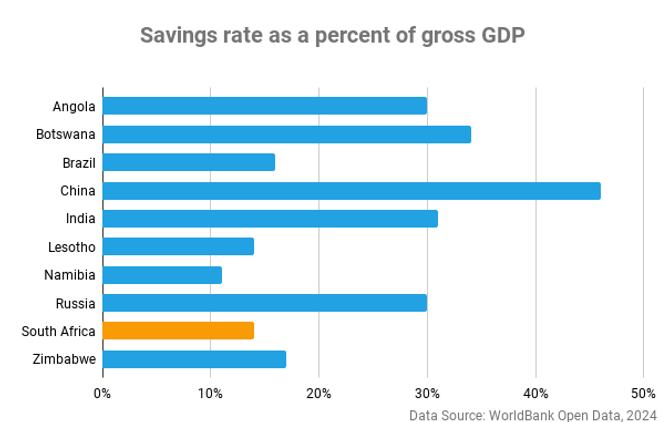

South Africa also lags behind many of its peers in gross savings rates. In 2023, South Africa’s gross savings rate was just 14%, compared to over 30% in countries like China, India, and Botswana. A country’s saving rate is a critical indicator of its economic resilience and long-term growth potential.

Savings also play a pivotal role in funding domestic investment, driving infrastructure development, business expansion, and job creation. When savings are insufficient, the country becomes increasingly dependent on foreign capital to fund its investments, which heightens its vulnerability to external shocks such as currency fluctuations or changes in global interest rates.

For households, low savings rates limit financial security and the ability to withstand emergencies like job losses or medical expenses. This contributes to rising debt levels and financial stress. Finally, inadequate savings reduce opportunities for wealth accumulation, exacerbating South Africa’s stark income and wealth inequality.

Insurance penetration is similarly low. The majority of South Africans are unable to afford traditional insurance products, leaving them vulnerable to financial shocks. In 2023, 48% of South Africans had funeral cover, the most common type of insurance, but other forms of coverage, such as life insurance (12%) and medical aid (7%), remain out of reach for most. Without these financial safety nets, many households are left exposed to significant risks that could derail their financial progress.

The low penetration of non-funeral insurance products points to a larger issue in the South African financial landscape: while access to financial services is high, the high costs associated with many essential products prevent meaningful participation for most South Africans.

Financial Inclusion is a pathway to equality and opportunity

In South Africa, financial inclusion has seen significant progress in terms of availability, with most people having access to formal banking services. However, the high costs of credit, savings, and insurance prevent many South Africans from fully benefiting from the financial system. Credit access is vital for wealth building, particularly through property ownership, but many South Africans still face barriers due to poor creditworthiness or limited financial literacy. Additionally, savings and insurance penetration remain low, leaving households vulnerable to financial shocks.

To truly improve financial inclusion in South Africa, efforts must focus on making financial products more affordable and ensuring that individuals use these services to build wealth and secure their futures. This will require addressing the affordability gaps and promoting financial literacy to empower South Africans to make the most of the financial tools available to them.

References:

-

FinMark Trust. 2024. FinScope Consumer South Africa 2023 Survey Launch. [Presentation]. Available: https://finmark.org.za/Publications/FinScope_SA_Consumer_2023.pdf

-

FinMark Trust. 2011. FinScope South Africa 2011. Available: https://finmark.org.za/system/documents/files/000/000/402/original/Survey_Highlights_2011.pdf?1614854200

-

National Credit Regulator. Credit Bureau Monitor: June 2024. Available: https://www.ncr.org.za/documents/CBM/CBM%20Q2%202024.pdf.

-

National Credit Regulator. Consumer Credit Market Report: June 2024. Available: https://www.ncr.org.za/documents/CCMR/CCMR%202024Q2.pdf.

-

Trading Economics. 2024. South Africa Household Saving Ratio. Available: https://tradingeconomics.com/south-africa/personal-savings#:~:text=Household%20Saving%20Rate%20in%20South,the%20third%20quarter%20of%202023.

-

World Bank Open Data. 2024. Available: https://data.worldbank.org/.